Story By Daniel Addo, PhD Candidate

In global finance, the most expensive mistakes are rarely caused by a lack of data. They are caused by a failure to interpret signals early enough. Nowhere is this truer than in Africa, where sovereign risk is still largely read through frameworks designed for economies that behave very differently.

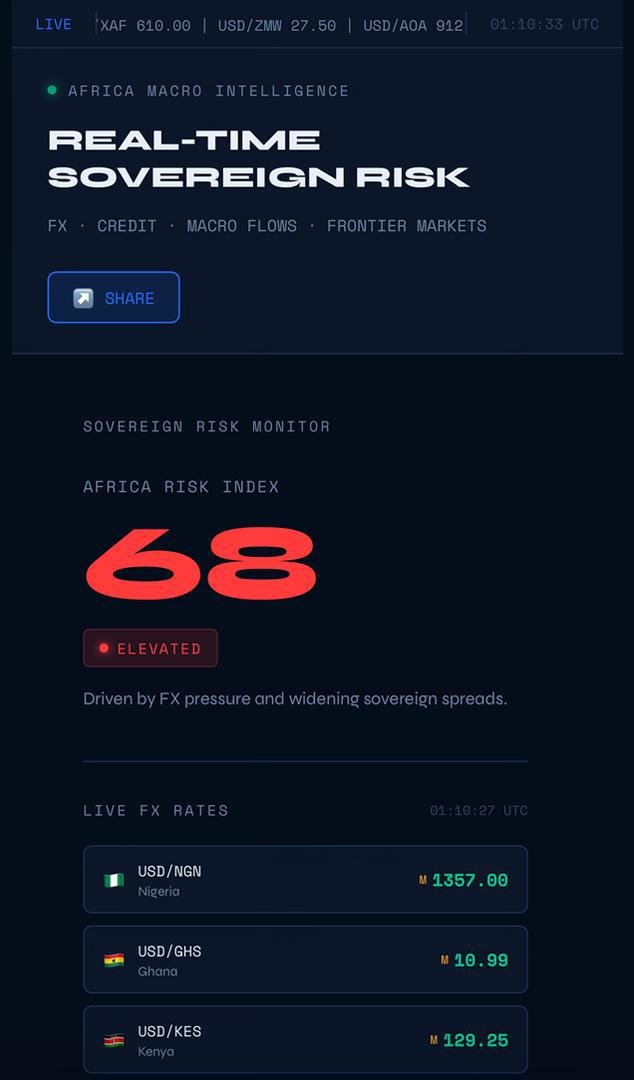

Lord Fiifi Quayle’s Africa Risk Index is an attempt to correct that mismatch. It does not reject traditional metrics debt ratios, fiscal balances, inflation but it reorders them. It asks a more practical question: how does risk actually show up on the ground before it appears in official data?

This shift is subtle but important. The deeper issue is not risk itself, but the persistent mispricing of uncertainty. In African markets, what cannot be easily observed is often what matters most; liquidity constraints, payment frictions, and the credibility of policy execution. These forces rarely appear cleanly in official statistics until much later. What Quayle’s framework does is make that uncertainty legible.

Conventional sovereign analysis, as practiced by rating agencies, is backward-looking by design. It validates stability after it has been achieved and flags distress once it has already materialised. By the time a downgrade happens, markets have often moved. The signal, in other words, arrives late.

Quayle’s framework works in the opposite direction. It focuses on what might be called “pre-data signals”—liquidity pressures in payment corridors, execution credibility in fiscal policy, and the consistency of a country’s access to external financing. These are not abstract indicators; they are observable frictions in how economies function day to day.

Recent analysis from his Africa Sovereign Credit Monitor illustrates this approach. Countries are not simply ranked by growth or debt sustainability, but by regime: expansion, stability, or stress. Ivory Coast, for example, is characterised by strong execution credibility and sustained market access, while Kenya reflects liquidity pressure and turnaround risk. The distinction is not cosmetic, it is predictive.

This is where the Africa Risk Index becomes most useful. It translates macroeconomics into market behaviour.

In African economies, risk does not always transmit cleanly through official channels. It leaks; through foreign exchange allocation systems, through delays in payments, through widening gaps between official and parallel markets. By the time these leakages are captured in GDP revisions or fiscal reports, the underlying dynamics are already entrenched.

A framework that captures these early distortions offers a meaningful edge. It allows investors, policymakers, and analysts to see stress forming before it crystallises into crisis.

Critics may argue that such an approach introduces subjectivity. That is partly true. But the greater risk lies in false precision; models that appear rigorous yet fail to capture how African economies actually operate. In environments where institutions are uneven and data lags are significant, qualitative signals are not a weakness; they are a necessity.

More broadly, the Africa Risk Index reflects a deeper intellectual shift. It treats African economies not as imperfect versions of developed markets, but as systems with their own logic; where informality, state capacity, and external dependency interact in complex ways.

This matters because capital is increasingly sensitive to narrative as much as numbers. Investors are not only asking whether a country meets fiscal targets; they are asking whether it can execute, whether it can maintain access to markets, and whether stress is building beneath the surface.

In that sense, Quayle’s contribution is not just analytical, it is interpretive. He offers a language for understanding African risk that is closer to how it is experienced in real time.

The challenge now is adoption.

For the Africa Risk Index to have lasting impact, it must move beyond proprietary research into broader institutional use. Policymakers could use it to identify pressure points earlier. Investors could integrate it into frontier market strategies. Even rating agencies, over time, may find value in incorporating elements of its signal-based approach.

Africa does not lack data. It lacks frameworks that read that data in context.

If the continent is to attract stable, long-term capital and avoid the repeated cycle of optimism and crisis it must develop tools that see risk as it forms, not after it has already arrived.

On that front, the Africa Risk Index is not just timely. It is necessary.

Signals Before Ratings: Why Africa Needs a New Risk Language